Understanding True New Car Price

True new car price – Navigating the new car market can be daunting, with a maze of prices and fees. This article clarifies the complexities of determining a vehicle’s true cost, helping you become a more informed buyer and achieve a fair price.

Defining “True New Car Price”

Source: cheggcdn.com

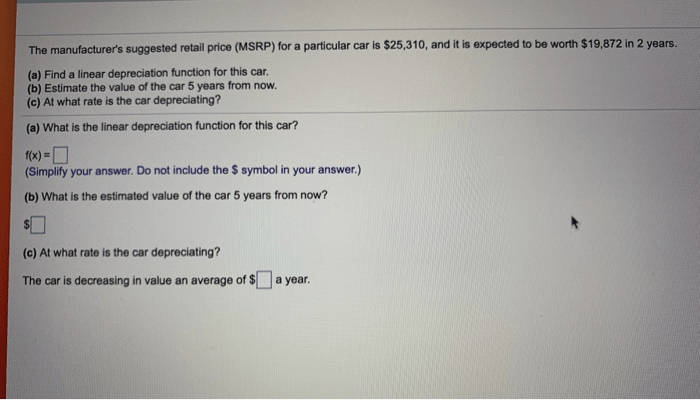

Determining a true new car price can be tricky, factoring in various fees and optional extras. A good example to consider is the tesla model y new car price , which itself varies based on configuration and location. Ultimately, understanding the true cost involves careful research beyond the manufacturer’s suggested retail price to avoid unexpected expenses.

The “true new car price” represents the final amount a consumer pays after negotiations, including all fees and charges. It differs significantly from the Manufacturer’s Suggested Retail Price (MSRP) and the invoice price.

The MSRP is the manufacturer’s suggested price, often higher than what consumers ultimately pay. The invoice price is what the dealership pays the manufacturer, serving as a baseline for negotiations. The actual price paid is influenced by several factors, including dealer incentives, rebates, financing options, and hidden fees.

Factors influencing final price negotiation include dealer incentives (profits they make), manufacturer rebates (money back from the manufacturer), financing options (interest rates and loan terms offered by the dealership or external lenders), and various hidden fees (document fees, processing fees, etc.).

Hidden fees such as destination charges, advertising fees, and dealer preparation fees can significantly inflate the final price. These are often added without clear explanation.

| Car Model | MSRP | Invoice Price (Estimate) | Typical Final Sale Price |

|---|---|---|---|

| Toyota Camry | $27,000 | $25,000 | $26,000 |

| Honda Civic | $24,000 | $22,000 | $23,000 |

| Ford Explorer | $35,000 | $32,000 | $33,500 |

Market Research and Data Sources

Source: autocheatsheet.com

Determining the true market value requires research. Reliable sources include Kelley Blue Book (KBB), Edmunds, and TrueCar, which provide average transaction prices for various car models and regions. These websites aggregate data from actual sales, offering a realistic picture of what consumers are paying.

Comparing prices across dealerships and locations involves using these websites, inputting your desired car specifications and location. This allows you to see price variations and identify potential bargains.

Organizing data from multiple sources helps illustrate price variations. For example, comparing KBB’s average transaction price with Edmunds’ data for the same car model in different states can reveal significant regional differences.

| Car Model | Year | Average Transaction Price (Source A) | Average Transaction Price (Source B) |

|---|---|---|---|

| Honda CRV | 2023 | $28,500 | $29,200 |

| Toyota RAV4 | 2023 | $30,000 | $30,800 |

Factors Affecting Price Negotiation

The dealer’s profit margin is a crucial factor. Dealers aim to maximize profit within a reasonable range. Supply and demand significantly impact pricing. High demand for a specific model often leads to higher prices, while low demand can result in discounts.

Negotiation strategies vary in effectiveness. Researching the market value beforehand strengthens your negotiating position. Being prepared to walk away can also be a powerful tactic.

Consumer credit scores directly influence financing options and overall price. A higher credit score typically leads to better interest rates, reducing the total cost of ownership.

Understanding Incentives and Rebates

Manufacturers frequently offer rebates and incentives to boost sales. These can include cash back, low-interest financing, or special lease deals. Choosing between leasing and purchasing significantly affects the true cost of ownership. Leasing generally involves lower monthly payments but higher overall costs over the long term compared to purchasing.

Financing options such as loans and leases impact the total price. Lower interest rates reduce the overall cost, while longer loan terms result in higher interest payments.

- Scenario 1: $3,000 cash back rebate + 2% interest rate loan = lower final price.

- Scenario 2: 0% APR financing but no rebate = potentially higher total cost due to higher monthly payments.

- Scenario 3: Lease with low monthly payments but higher overall cost over the lease term.

Transparency and Consumer Protection

Source: alamy.com

Dealerships sometimes employ deceptive tactics, such as adding unnecessary fees or misrepresenting financing options. Consumers should be aware of these practices and take steps to protect themselves.

Protecting yourself involves careful review of all documents, negotiating transparently, and seeking clarification on any unclear terms. Understanding the terms and conditions of financing agreements is crucial.

- Research the car’s market value before visiting a dealership.

- Compare prices from multiple dealerships.

- Carefully review all documents before signing.

- Understand the financing terms completely.

- Don’t be pressured into making a quick decision.

Illustrative Examples of Price Variations, True new car price

Let’s consider a hypothetical scenario: A new Honda Civic has an MSRP of $24,000. After negotiations, including a manufacturer rebate of $1,000 and a favorable interest rate, the final sale price could be $22,500. This illustrates the difference between MSRP and the true price.

In another scenario, during a period of low demand for a specific car model, a consumer successfully negotiates a $2,000 discount, achieving a price significantly below the average transaction price.

Choosing a 72-month loan instead of a 60-month loan will result in lower monthly payments but significantly higher total interest paid over the loan term. This demonstrates the impact of financing choices on overall cost.

Adding hidden fees, such as a $500 dealer prep fee and a $200 document fee, increases the final price by $700. This illustrates how hidden fees inflate the final price, increasing the total cost beyond the negotiated price.

FAQ Resource: True New Car Price

What is the difference between MSRP and invoice price?

MSRP is the manufacturer’s suggested retail price, while the invoice price is what the dealership pays the manufacturer. The difference represents the dealer’s potential profit margin.

How can I find out the average transaction price for a specific car model?

Websites like Kelley Blue Book (KBB) and Edmunds provide average transaction prices based on real-world sales data. These resources often allow you to filter by location and model year.

Are there any legal protections against deceptive sales tactics?

Yes, many consumer protection laws exist at both the state and federal levels to prevent deceptive advertising and unfair sales practices. It’s crucial to understand your rights as a consumer.

What is the best time of year to buy a new car?

The end of the month and the end of the quarter are typically good times to buy a new car as dealerships often try to meet sales quotas.